.svg)

.svg)

.svg)

.svg)

.svg)

.svg)

What is overfitting?

← Back to FAQ

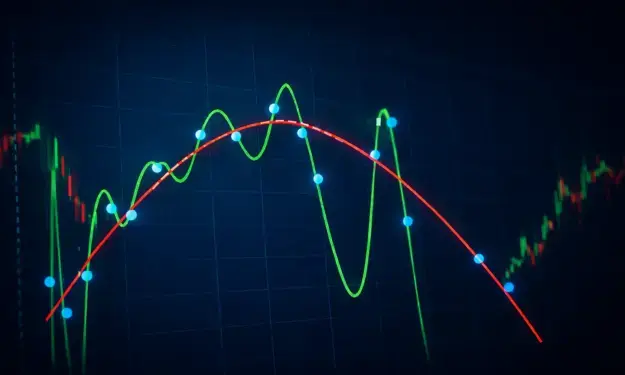

Overfitting occurs when a model or strategy is too closely tailored to historical data. It means the model learns patterns that exist in past data but do not represent real underlying relationships. As a result, the model may perform well on past data but poorly on new or unseen data.

Overfitting can make a model appear more accurate than it actually is.

In finance and quantitative trading, overfitting often happens when a strategy is optimized too much using historical market data. By adjusting many parameters, the model may capture random noise instead of meaningful trends.

This creates a strategy that seems profitable in backtests but fails when applied in real market conditions. To reduce overfitting, analysts often test models on separate datasets and use simpler models that focus on robust patterns rather than perfect historical accuracy.

Short example:

Suppose a trader builds a trading algorithm using ten years of historical stock market data.

The trader adjusts the strategy many times until the backtest shows very high profits.

However, when the strategy is used in live trading, the results are disappointing because the model was fitted too closely to the past data. The strategy captured random historical patterns instead of reliable market behavior.

Disclaimer: Investing brings risks. Our analysts are not financial advisors. Always consult an advisor when making financial decisions. The information and tips provided on this website are based on our analysts' own insights and experiences. Therefore, they are for educational purposes only.